The power market: three applications, one ecosystem

In a new report 'Power Electronics Market 2026-2036: Data centres, Electric Vehicles, and Renewables', IDTechEx has tracked innovation trends across the power electronics market, showing how demand is growing rapidly driven largely by demand EVs and data centres.

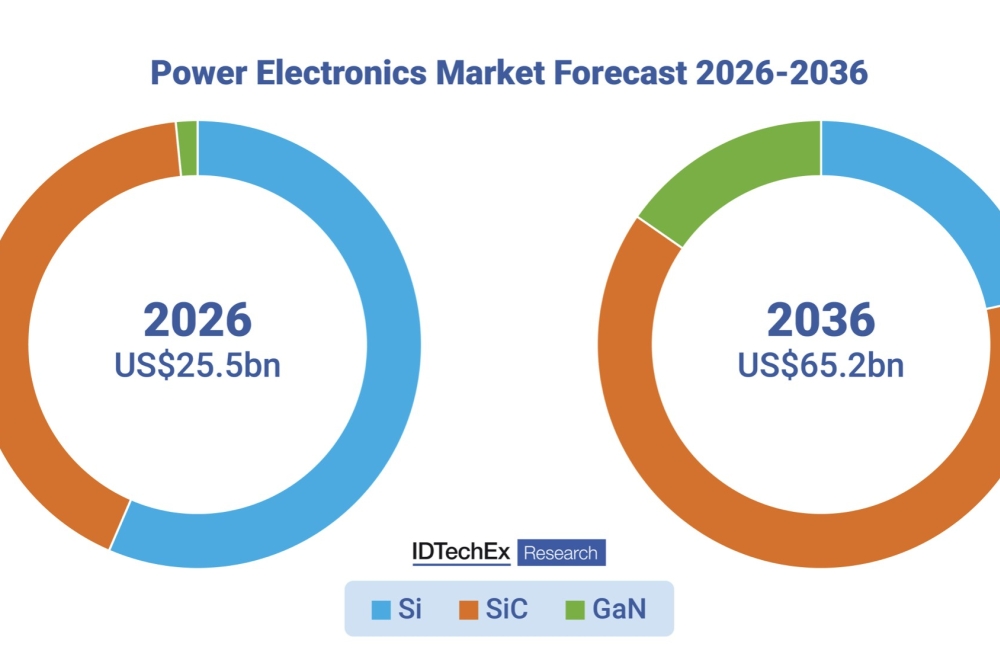

According to IDTechEx forecasts, the power electronics market will exceed $65 billion by 2036, representing a 10 percent CAGR over the next decade.

While silicon IGBTs have remained the dominant power device of choice for the past 20 years of traction inverters, alongside other silicon power devices for the onboard charger and DC-DC converter, wide bandgap technologies such as SiC MOSFETs occupy a significant and growing portion of the EV power electronics market.

IDTechEx predicts that SiC MOSFETs will form the majority of the EV traction inverter market by 2036, as well as the majority of the onboard charger and DC-DC converter market. The high-temperature operation, faster switching speeds, and smaller form factor lead to improved efficiency, as well as weight and volume savings that ultimately support increased range and EV performance.

GaN has significant potential in EVs, but the development of automotive GaN depends on proof of its long-term reliability in an EV environment, as well as its ability to operate at high voltages for 800V EV power architectures.

Data centres: the shift to 800VDC power architecture

The data centre industry has transformed since the widespread adoption of AI in 2023. AI models are becoming increasingly complex and require larger computational power for training. This has resulted in rapid development of new generations of AI chips, which draw higher levels of power. The AI data centre power electronics industry must adapt to support future generations of AI training.

Wide bandgap semiconductors are expected to become more prevalent in power supply units (PSUs) for data centres, as well as for point-of-load power conversion. The increased switching frequency and breakdown voltage of SiC and GaN enable more powerful and efficient power conversion devices in smaller form factors, while still maintaining the necessary reliability for AI training and inference. IDTechEx’s report “Power Electronics Market 2026-2036: Data centres, Electric Vehicles, and Renewables” includes a 10-year forecast of Si, SiC and GaN in data centres, predicting considerable uptake of GaN over the next ten years, especially for PSU and point-of-load power conversion.

At the same time, data centre power architecture will undergo a paradigm shift in the coming years, moving from AC power delivery to an 800VDC (HVDC) data centre power architecture. This transition is expected to simplify data centre power electronics, reducing the number of power conversion stages and points of failure. At the same time, this will increase overall data centre efficiency and enable the 1MW rack expected by the end of the decade.

This report includes a 10-year data centre power architecture forecast; IDTechEx expects that 800VDC will become the dominant power architecture for new AI data centres over the forecast period. In this report, IDTechEx compares the data centre power electronics market with the EV power electronics market, identifying key cross-overs and shared innovations between the two.

Wind Energy: Silicon slows WBG adoption

While a relatively small segment of the overall power electronics market, power electronics for wind energy represents an important contrast to the EV and data centre industries. With even higher power ratings, more challenging conditions (extreme temperature fluctuations, high humidity, and salt spray), and significant costs in the case of failure, the wind power electronics industry has been hesitant to adopt newer wide bandgap power electronics innovations, opting instead for the long-proven reliability of silicon technology.

Tracking partnerships between wind OEMs and SiC suppliers, and through IDTechEx’s conversations with players such as Hitachi Energy, IDTechEx has produced a 10-year forecast of Si and SiC demand for wind power converters, forecasting a steady adoption of SiC in the wind power electronics industry over the next ten years. The adoption of SiC in the wind industry represents a shift in wide bandgap technology; its long-term reliability has been sufficiently proven in harsh environments to extend its range of applications into renewable energy.

From the sterile environment of an AI data centre, where strong demand for increased power density to train next-generation AI models is driving investment in power electronics innovation, to wind turbine power converters, where strong cost pressure and reliability considerations are paramount, power electronics innovations look very different across industries. With applications so different and yet so inter-related, a cross-industry approach must be taken to understand how innovations in one field affect others.